Travel Trends - July 2025 Curaçao’s Tourism Statistics

- David Hecht

- Jul 17, 2025

- 5 min read

Just when you thought things would quiet down... Curaçao typically settles into a quieter summer rhythm in June. Not this year! June 2025 delivered a very different story, roaring to life with 57,412 stay‑over arrivals, eclipsing last June’s 50,110 by 14.6% and outpacing June 2023's 44,368 by 29.3%. June’s total not only set a new June record but shattered the seasonal norm of roughly 47,000 arrivals seen over the past three years, reflecting an unprecedented shoulder‑season surge.

Europe and North America remained the largest contributors, supplying 19,554 and 17,997 visitors respectively, while South America and the Caribbean delivered outsized YoY gains of 20% and 25%. More striking still, the average length of stay climbed from 7.2 nights last June to 7.7 nights this year, suggesting guests are not only arriving in greater numbers but lingering longer, soaking up Curaçao’s culture, cuisine and coastline. Even day‑tripper traffic marked a triumphant return. 3,253 short‑stay visitors, impressive 80% jump, rediscovered the country’s beaches and day‑use offerings.

Colombia once again stole the spotlight with its repeat June surge; 5,770 arrivals, up from 5,290 last year, vaulting the country into Curaçao’s top three source markets. This pattern isn’t accidental. Mid‑year school breaks dovetail with Father’s Day weekend, regional music festivals drive group bookings and direct Avianca connections make week‑long family retreats seamless. In June, Colombian visitors stayed an average of 5.4 nights, with 59 percent choosing resort accommodations, underscoring their appetite for comfortable, family‑friendly stays. And the momentum is set to grow: LATAM Airlines Colombia will launch a new, three‑times‑weekly Bogotá–Curaçao route on December 2nd, promising even greater ease of travel for both leisure and business guests.

Trends & Opportunities

Meanwhile, other markets told equally compelling stories. After peaking in May, Brazilian arrivals normalized to 2,482 in June (–20% MoM), while Canadian visitors surged 30% YoY. An impressive increase,

though a jump to only 878 travelers driving an 8% ytd gain. Cruise traffic enjoyed a boost as twelve ships came to port vs eight last June. YTD, the number of arrivals via cruise ships are down a marginal 5% from last year’s pace. Taken together with the dramatic resurgence in day‑trippers, these shifts reveal not just growth in sheer numbers but a rich diversification of traveler profiles, inviting operators to tailor experiences for multigenerational holidaymakers, cultural explorers lingering for a week, and spontaneous weekend wanderers alike.

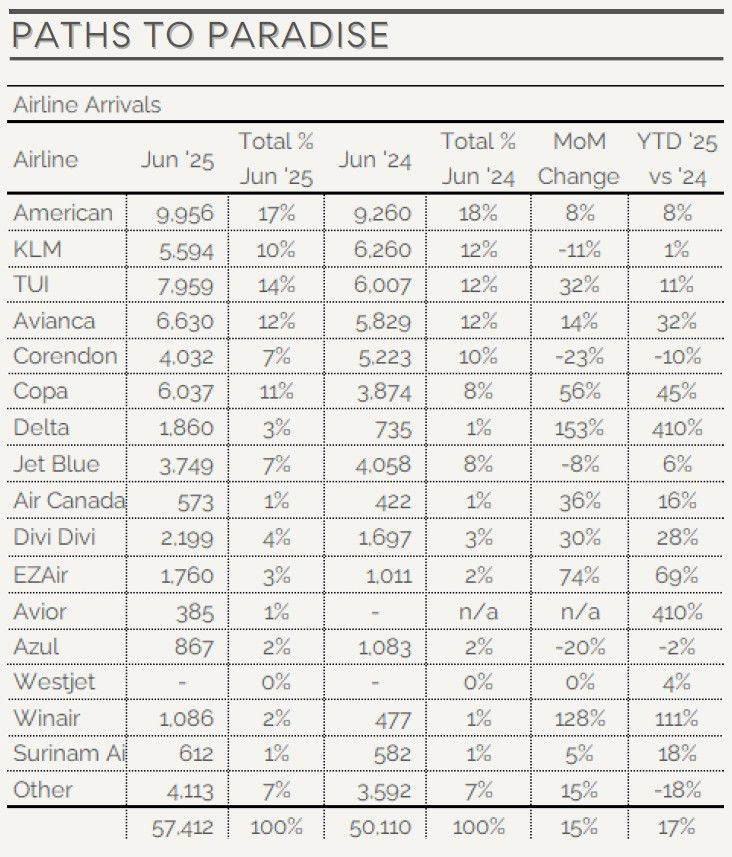

Turning to airlift, legacy carriers like American Airlines underpinned volume with 9,956 June arrivals (an 8% MoM increase), while Delta’s expanded U.S. schedule fueled a 153% MoM jump to 1,860 arrivals and a 410% ytd surge. Regional heavyweights Avianca and Copa posted MoM gains of 14% and 56% respectively and niche operators such as EZAir (+ 74 % MoM; + 69 %ytd) and Divi Divi (+ 30 % MoM; + 28 % YTD) captured regional bookings and spontaneous weekend escapes.

Amid this dynamic airlift landscape, another noteworthy shift has been unfolding on the distribution front. Direct channels (bookings with hotels and airlines) account for nearly 31% of all stay‑over reservations while OTAs captured 119K (30%) and traditional travel agents 91K (23%). This strong showing underscores rising guest loyalty and the premium travelers place on rate guarantees, flexible change policies and loyalty benefits

when they book direct. For hoteliers and airlines, each direct reservation sidesteps the typical 15–20 % OTA commission, translating into meaningful cost savings and higher net revenue per booking and it underlines why those larger players are ramping up loyalty programs and flexible‑change guarantees.

By contrast, individual homeowners currently live largely in the OTA-dominated world, with their own direct channels buried in the “Other” and “Unknown” segments. That gap represents a real opportunity. By building user‑friendly booking widgets, offering owner‑direct perks (e.g. waived fees, welcome packages) and collecting guest data, homeowners can tap into the same 31 % direct‑booking trend, capturing higher‑margin, more loyal guests without reliance on third‑party platforms.

Netherlands (16,390 visitors | ↑6.3 % YoY, ↑4.8 % YTD)

Dutch guests continue to lead in length of stay, averaging 11.66 nights in June, up from 11.35 nights a year ago, contributing 191,180 room-nights (+ 8% YoY).

As a reliably long-stay market (now accounting for 41% of YTD arrivals and 56% of YTD nights), the Netherlands underpins mid-week occupancy and average daily rate.

*** Best suited for premium, residential-style properties offering space, privacy and amenities geared to extended stays.

United States (17,119 visitors | ↑14.8 % YoY, ↑22.1 % YTD)

U.S. arrivals jumped 14.8% to 17,119 and room-nights rose 15% to 102,934. Avg stay of 6.01 nights.

This short-to-mid-length segment drives high turnover and consistent weekend demand, especially from family and friends-and-family (VFR) travel.

***Ideal for well-appointed, hotel-style villas and turnkey rental homes with efficient turnover and service-oriented amenities.

Canada (878 visitors | ↑30.1 % YoY, ↑11.6 % YTD)

Canadian arrivals rebounded sharply (+30% YoY) to 878, generating 7,007 room-nights (+ 21%), with stays averaging 7.98 nights.

After slipping in early 2025, Canada’s return signals renewed confidence among this long-weekend and early-summer market.

***Comfort, familiarity and reliable service remain key. Properties with home-like touches and clear service standards perform best.

Colombia (5,770 visitors | ↑9.1 % YoY, ↑8.2 % YTD)

Colombia’s repeat June surge hit 5,770 arrivals (+9%), producing 31,347 room-nights (+6%) at an average of 5.43 nights.

Driven by mid-year school breaks and festival calendars, this market skews toward quick, cost-efficient bookings.

***Optimize for flexible minimum-stays, streamlined booking processes and weekend-oriented packages around regional holidays.

Brazil (2,482 visitors | ↓19.6 % YoY, ↓5.3 % YTD)

Brazilian arrivals eased to 2,482 (–19.6%), with nights down 22% to 16,419. Avg. stay was 6.62 nights.

This return to normalization mirrors typical shoulder-season patterns after strong May performance.

***Offer special discounts for groups or longer stays during the quieter months. Brazilian travelers still make up a key share of bookings for certain properties.

Takeaways

There is no denying that June’s tourist data impressed. As we move past the uptick and look towards the rest of the year, it’s clear though, that Curaçao’s seasonality won’t disappear overnight. It is equally clear, however, that the seasonality is softening. The traditional high season (December through February) remains the busiest time, yet we’re now seeing reliable demand stretch well into late spring and even early summer, trimming what used to be well pronounced lulls. For homeowners and small‑portfolio investors, this means that calendars may fill more evenly. Consider modest rate adjustments to smooth out gaps between December peaks and late‑year slumps and introduce tiered minimum‑stay rules that ease for mid‑year school breaks and shoulder‑season weekends.

At the same time, new demand pockets are emerging. June school holidays, September’s cultural festivals and even late‑summer events are beginning to look more like reliable, source‑market drivers than one‑off bumps. To capture these pockets of demand, think about targeted promotions like family‑friendly packages in June, festival‑tie‑ins later in the year and modular add‑ons that can be switched on or off without overhauling your base rate.

Above all, adopt a balanced strategy. One that acknowledges the enduring strength of the winter sun market and leans into the supplementary spikes. By smoothing rates across twelve months, embracing flexible stay requirements and crafting time‑specific offers, you’ll have a better chance at reducing deep lulls, protect your average daily rate and build a more predictable, year‑round revenue stream. It’s not about chasing every guest at any cost. It’s about matching your property’s availability and pricing to the island’s evolving demand.

Comments